Audi Car Finance

Audi Car Finance  BMW Car Finance

BMW Car Finance  Ford Car Finance

Ford Car Finance  Kia Car Finance

Kia Car Finance  Land Rover Car Finance

Land Rover Car Finance  Mercedes Benz Car Finance

Mercedes Benz Car Finance  Nissan Car Finance

Nissan Car Finance  Peugeot Car Finance

Peugeot Car Finance  Tesla Car Finance

Tesla Car Finance  Toyota Car Finance

Toyota Car Finance  Vauxhall Car Finance

Vauxhall Car Finance  Volkswagen Car Finance

Volkswagen Car Finance PCP vs HP: Which Car Finance Option Is Right for You?

PCP vs HP: A Complete Comparison

When it comes to financing a car in the UK, two options dominate the market: Personal Contract Purchase (PCP) and Hire Purchase (HP). Both allow you to spread the cost of a vehicle over monthly payments, but they work quite differently. Understanding these differences is crucial to choosing the option that best fits your lifestyle and budget.

How PCP Works

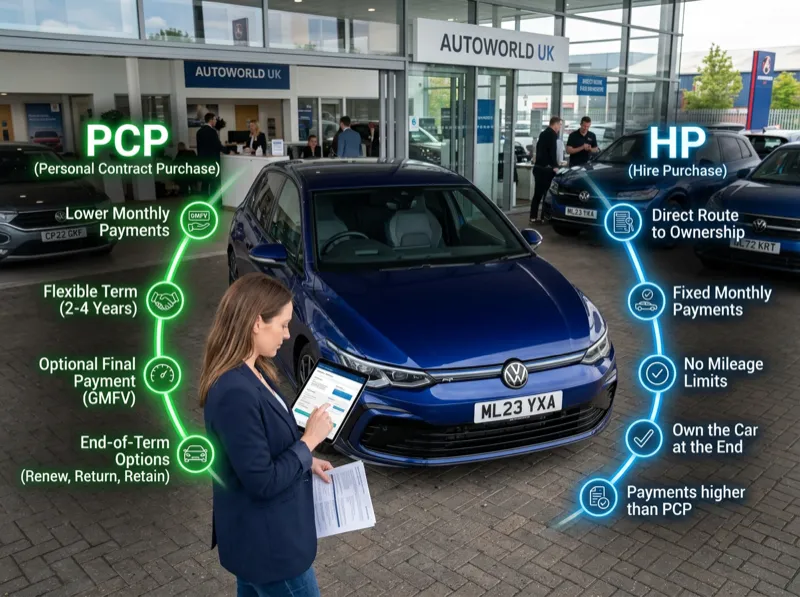

With PCP, your monthly payments cover the depreciation of the vehicle rather than its full value. At the start of the agreement, the lender sets a Guaranteed Minimum Future Value (GMFV), which represents the car’s predicted worth at the end of the term.

Your monthly payments are calculated based on the difference between the car’s price (minus any deposit) and the GMFV. This means PCP payments are typically lower than HP payments for the same vehicle.

At the end of the agreement, you have three options: return the car, pay the balloon payment to own it, or use any equity as a deposit on a new car.

How HP Works

Hire Purchase is more straightforward. You pay a deposit (optional in some cases) and then make fixed monthly payments over an agreed term. Once all payments are made, you own the car outright. There is no balloon payment and no mileage restrictions.

HP monthly payments are higher than PCP because you are paying off the full value of the vehicle, but at the end of the agreement, the car is yours without any further costs.

Key Differences at a Glance

Monthly payments: PCP is typically lower because you are only paying for depreciation. HP is higher because you are paying off the full value.

Ownership: With HP, you own the car once all payments are made. With PCP, you only own the car if you choose to make the final balloon payment.

Mileage: PCP agreements come with mileage limits, and exceeding them results in excess mileage charges. HP has no mileage restrictions.

Flexibility: PCP offers more end-of-term options, including handing the car back or upgrading. HP is a simpler own-the-car arrangement.

Deposit: Both can be arranged with no deposit, though a deposit will reduce monthly payments in either case.

Total cost: If you intend to keep the car, HP is usually cheaper overall because you avoid the balloon payment and the interest charged on it.

When PCP Makes More Sense

PCP is ideal if you:

- Want lower monthly payments

- Like to change your car every two to four years

- Drive a predictable number of miles each year

- Want access to newer, higher-specification vehicles

- Are not concerned about owning the car outright

Many drivers use PCP as a way to always have a relatively new car without the large financial commitment of outright purchase. It is particularly popular among those who view a car as a practical tool rather than a long-term asset.

When HP Makes More Sense

HP is the better choice if you:

- Want to own the car at the end of the agreement

- Do a high number of miles each year

- Plan to keep the car for many years

- Prefer a simple, no-surprises agreement

- Want to modify the vehicle once it is yours

HP is often favoured by drivers who rack up significant mileage, as there are no per-mile charges to worry about. It is also popular with people who want the security of knowing the car will be theirs once the payments are complete.

Which Is Cheaper Overall?

The answer depends on your plans. If you intend to hand the car back at the end of the agreement, PCP is almost always the more affordable option because you only pay for the depreciation.

However, if you want to keep the car, HP is generally cheaper in total. With PCP, the balloon payment adds a significant lump sum to the overall cost, and you will have been paying interest on that amount throughout the agreement even though you did not benefit from it until the end.

Can You Get Both with Bad Credit?

Yes. Both PCP and HP are available to customers with less-than-perfect credit. Specialist lenders exist for both finance types, though the interest rates may be higher. At Happy Motor Finance, we work with lenders across the spectrum to find the best deal for your circumstances, regardless of your credit history.

Our Recommendation

There is no one-size-fits-all answer. The best choice depends on your budget, driving habits, and whether ownership matters to you. We recommend comparing quotes for both PCP and HP on your desired vehicle so you can see the real numbers side by side. Happy Motor Finance can provide quotes for both options with a single soft credit check. Get in touch today.

Happy Motor Finance

FCA Authorised (FRN 989250) · SAF Approved

Our team of FCA-authorised finance specialists help people across the UK get behind the wheel, regardless of credit history. We act as a credit broker, searching a panel of lenders to find the right deal for you.

Ready to Get Started?

Apply for car finance today and get a decision in minutes.

With no impact to your credit score*

We act as a credit broker, not a lender

Representative example: borrowing £6,500 over 5 years with a representative APR of 16.9%, an annual interest rate of 16.9% (Fixed) and a deposit of £0.00, the amount payable would be £161.19 per month, with a total cost of credit of £3,171.55 and a total amount payable of £9,671.55. This is an example only, lender fees may apply. The exact rate you will be offered will depend on your circumstances. All finance subject to status.

*After completing the application, lenders will perform a “soft search” that will not affect your credit score. Should you get an offer of finance and wish to proceed, the lender will then perform a “hard search” of your credit file. Finance acceptance is not guaranteed, please click the following link for more information: Initial Disclosure Document